By Dr. Housing Bubble | 12 June 2008

I was having a conversation with someone last week regarding his home equity line being shut down. He was rather distraught and frustrated by the sudden move of the lender to close off his line due to market conditions here in California. "How can they do that? They have no right to take away my hard earned money!" Aside from restraining myself from smacking him upside his head I did ask him how he had 'earned' that money that was now gone. "My home equity was my money. The bank has no right to close off access to my money." Welcome to the new mentality of wealth in our nation.

This simple conversation is the tip of the iceberg of the challenge that is now confronting our nation. In the past few decades, Americans have arrived at the current distorted point of reality where alternate universes collide and somehow debt or 'paper profits' are now the equivalent of wealth [[but weren't the banks and all other financial institutions treating it as such, world-wide? : normxxx]] I should actually clarify that last statement in light of the above conversation about home equity lines being shut down:

|

That is a very important point and once you grasp this knowledge, you can understand why we are in the predicament we are in. Today, retail sales numbers perked up and the market initially came out of the gate with guns-a-blazing. That is until folks stopped for two seconds and did the current economic math:

A: If all recent data is showing us that consumers are tapped out.

B: Home prices are still declining and foreclosures are rising.

C: Consumer inflation is hitting on every front.

D: Then how can Americans still be spending?

Let me show you how:

|

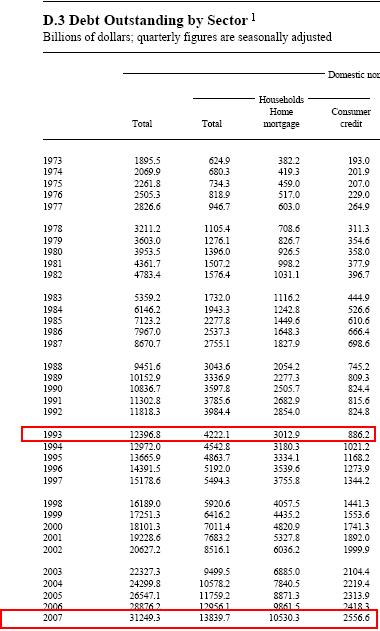

The above article was posted in January; now we are lots closer to $1 trillion in revolving consumer debt out there. And the more ominous problem is that defaults are rising in this area. So, due to the lack of wage growth, people were [are] using leverage via mortgages and consumer debt to bridge the Joneses gap. Take a look at the massive explosion in mortgage and consumer debt over the past 20 years:

Source: Fed Flow of Funds Report, June 2008

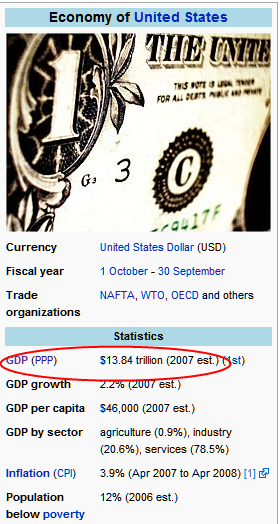

It is rather shocking that American households have approximately $13.84 trillion in debt obligations. In 1993, this number was at $4.2 trillion so we’ve nearly triple our national household debt in the matter of 15 years. That $13.84 trillion is a very large number and to put that into context, the estimate GDP for the entire United States for 2007 was $13.84 trillion:

Source: Wikipedia

We spent every last penny! Is it any wonder Americans have a negative personal savings rate? You really have to wonder how people can spend more than they earn but that is essentially the way we as a nation have been living for the past decade. This housing bubble fueled by the debt bubble was only a logical extension of the cultural financial neurosis. The great majority of the public started associating the ability to access credit with true financial prosperity. Well as we all now know, anyone with a pulse and one tooth was able to get a large mortgage in California by simply making things up. Need we remind you of the farmer making $14,000 a year with access to a $720,000 loan? Or what about the hundreds of credit card offers Americans receive each year in the mail? When debt is no longer seen as a necessary evil and, indeed, as a sign of wealth, new definitions take hold of mass psychology.

Take a look at this ad during the heyday of the housing bubble:

"Chances are, you’ll sell your home before we sell your mortgage." Is this some sort of race? The underlying implication of course is you’ll make so much equity in a few short years that you’ll be selling your current McMansion for a double whopper McMansion so why worry yourself with whether they sell your mortgage off to some foreign investor. These ads only spoke to the distorted psychology of consumers who thought access to a $500,000 mortgage meant that they had access to a $500,000 net worth.

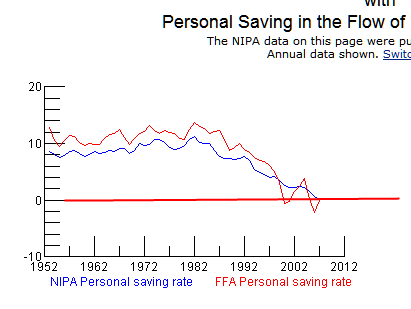

In a way, it allowed consumers to put on the bourgeois costume for a few years and feel like a million bucks even though they were drowning internally by suffocating debt. Think this isn’t the case? Take a look at the below charts:

Click Here, or on the image, to see a larger, undistorted image.

That is why at the height of pseudo prosperity and the pinnacle of the housing bubble, Americans had for the first time crossed the negative savings barrier. This is the perfect example of watering down the definition of wealth in our country; collectively as a society people started having an aversion to saving money and a liking to debt. This of course is a major problem and no country can survive in the long run with crushing amounts of debt. I don’t care what kind of math political parties want to sell you but there is no way a country can be prosperous in the long run by running larger and larger deficits.

This implosion of the credit (debt) markets is simply a decade long debt ponzi scheme that can go on no longer. Consumer psychology still can’t understand why fuel is rising or why everything from education to groceries are costing much more. The perfect scheme was to con people into believing that going into debt, meaning you were spending tomorrow’s dollars today, was somehow a prudent way toward wealth. And the entire idea of savings lost its allure. In fact, society punished savers implicitly. For much of the past, if you bought a home folks knew that you had the diligence and restraint to hunker down for 2 or 3 years and put off conspicuous consumption for a larger goal such as a home. That entire romanticism of saving went out the window when anyone and everyone was getting BMWs and McMansions with zero down.

In fact, if you were renting and saving and trying to be frugal, you were seen as an outcast and a bum because you just missed out in a home that just went up $50,000 in one years simply because everyone was smoking the housing peyote. I wonder how many people had a kitchen conversation like this circa 2003:

Spouse A: "We should buy a home. The Perma Bulls down the street bought a home last year and they now have $50,000 in equity."

Spouse B: "But it doesn’t make sense. How can a home be worth $50,000 more if they didn’t do anything?"

Spouse A: "Well here we are saving and all we’ve been able to save in our 2% savings account is $15,000. What if homes go up $50,000 again next year?"

Spouse B: "That can’t be because that makes no economic sense. Prices have got go up for some fundamental reason."

Spouse A: "I heard that they got a home equity line and took a trip to Europe. Isn’t that great and fantastic? We actually make a bit more than they do but why do we live and feel poorer?"

Spouse B: "I don’t know. It just doesn’t make sense. I feel uncomfortable going into that large amount of debt. Why is that?"

Spouse A: "Because you’re stupid?"

Spouse B: "No. You are stupid you moron; you don’t understand the difference between net worth and being in debt."

Spouse A: "Isn’t wealth about what you can buy? We don’t take fancy trips or even have our own home! You are the true idiot, you financial midget with no home."

Spouse B: "I hate you."

Spouse A: "I’m leaving you."

Spouse B: "Go ahead— and take the dog while you’re at it. I always hated how he looked at me anyways."

What a lovely and heart warming story don’t you think? As you can see from the above sign, many people did have a conversation like this, except that in our story above, the couple parted their ways because of diverging financial outlook. But from that lawn sign, we can see that those folks unfortunately realized that selling a home in a busted bubble is no easy task.

This is the real deal here folks. We are shifting back whether we want to or not. The real psychological shift that is unfolding is the ability to break down wants and needs. A big gas guzzling car is a want and many folks are now painfully realizing this. A large crushing mortgage for a McMansion is a want. Food, a basic roof over your head, and education are needs. Time to get these equations recalibrated before the market recalibrates them for you.

ߧ

Normxxx

______________

The contents of any third-party letters/reports above do not necessarily reflect the opinions or viewpoint of normxxx. They are provided for informational/educational purposes only.

The content of any message or post by normxxx anywhere on this site is not to be construed as constituting market or investment advice. Such is intended for educational purposes only. Individuals should always consult with their own advisors for specific investment advice.

No comments:

Post a Comment